Single-entry bookkeeping is one of the simplest accounting methods available, particularly favored by small businesses and sole proprietors for its straightforward approach. In essence, it involves recording each financial transaction only once — usually as a single entry in a cashbook or ledger. This method primarily focuses on cash inflows and outflows, making it ideal for businesses with uncomplicated financial transactions.

For instance, a local bakery might maintain a single-entry system categorizing daily cash sales, expenses for ingredients, and employee wages. This way, they can easily track their cash position without the complexities involved in comprehensive accounting systems.

While single-entry bookkeeping is accessible and easy to manage, it comes with its own set of pros and cons:

Advantages:

Limitations:

Ultimately, while single-entry bookkeeping can serve small entities well, it’s essential to recognize when to consider a shift towards more comprehensive systems, particularly as a business evolves.

Double-entry bookkeeping, often recognized as the gold standard in accounting, revolutionized financial record-keeping. This system operates on the fundamental principle that every financial transaction affects at least two accounts, ensuring that the accounting equation (Assets = Liabilities + Equity) remains in balance. This method is attributed to Luca Pacioli, the Father of Accounting, whose work in the late 15th century laid the groundwork for modern accounting practices.

Imagine a small business owner purchasing inventory. In a double-entry system, this transaction would simultaneously affect the inventory account (an asset increase) and the cash account (an asset decrease). By maintaining this dual perspective, businesses can achieve greater financial accuracy and clarity.

The principles of double-entry bookkeeping hinge on several key components that ensure accurate financial reporting:

To illustrate the process:

Double-entry bookkeeping is vital for businesses aiming for growth, as it facilitates comprehensive financial analysis and promotes transparency in financial reporting. This system not only safeguards against errors but also establishes a foundation for sound financial decision-making.

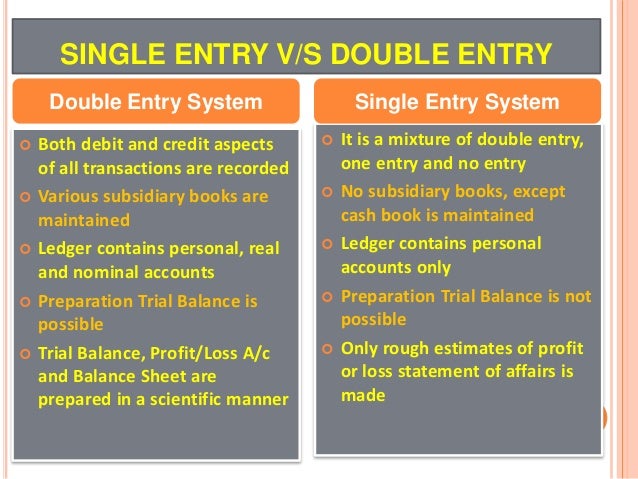

When comparing single-entry and double-entry bookkeeping, one of the most significant differences lies in their accuracy and complexity. Single-entry bookkeeping may seem straightforward, but this simplicity can lead to inaccuracies. With only one entry per transaction, it becomes easy to overlook mistakes.

For instance, if a business owner forgets to record an expense, the financial picture could appear healthier than it is, leading to misguided decisions. Consequently, single-entry systems often reveal only limited insights into the financial health of the business.

In contrast, double-entry bookkeeping introduces an increased level of accuracy through its dual-recording system. Each transaction impacts two accounts, creating a built-in check. This method, while more complex, reduces the likelihood of errors since discrepancies in the entries directly indicate issues that need addressing.

Key Points:

The ability to analyze finances differs significantly between these two systems. Single-entry bookkeeping serves basic needs. It provides a snapshot of cash flow but does not allow for deeper financial insights. As a result, a business using this method may struggle to gain insights into profitability, growth opportunities, and potential risks.

On the other hand, double-entry bookkeeping is equipped for comprehensive financial analysis. It enables businesses to generate detailed financial statements, such as balance sheets and income statements, which are crucial for informed decision-making. With this method, entrepreneurs can quickly assess performance metrics like profit margins and cash flow trends.

Additional Benefits of Double-Entry:

Overall, while single-entry bookkeeping may be sufficient in the early stages of a business, as complexity grows, so does the need for a more sophisticated system like double-entry bookkeeping to provide meaningful financial insights.

One of the most compelling advantages of double-entry bookkeeping is its inherent ability to detect and prevent errors. In a single-entry system, mistakes can go unnoticed due to its simplistic format; a missed entry might lead to significant discrepancies that only surface during audits or cash flow crises.

Consider this scenario: A small coffee shop uses single-entry bookkeeping, neglecting to record a $200 utility bill. The owner believes they have $1,000 in cash, when in reality, the actual amount is closer to $800. Such oversights can quickly snowball into larger financial problems, affecting purchasing decisions and payroll.

In contrast, double-entry bookkeeping employs a mechanism that balances each transaction by recording it in two accounts. This dual approach makes it more difficult to overlook errors. If the debit and credit do not align, it signals an issue that demands further investigation. Thus, double-entry systems remarkably enhance the overall integrity of financial records.

The advantages of double-entry bookkeeping extend beyond accuracy into the realm of financial reporting. Businesses that implement double-entry systems can generate detailed financial reports, such as profit and loss statements, balance sheets, and cash flow statements. These documents are crucial for understanding a company’s financial performance and are often required when seeking loans or investors.

For example, a retail store using double-entry bookkeeping can analyze its sales revenue, expenses, and net income in various ways, allowing for effective trend analysis. This thorough reporting can support strategic planning and help businesses make informed decisions regarding budgeting, marketing, and growth.

Benefits of Enhanced Reporting:

In conclusion, the advantages of double-entry bookkeeping in terms of error detection and financial reporting aptly demonstrate why businesses aiming for growth and stability should consider transitioning from single-entry systems.

When considering the implementation of a bookkeeping system, the first step is choosing the right platform that fits the unique needs of your business. Various software options are available, ranging from simple spreadsheets to comprehensive accounting software tailored for double-entry systems.

For instance, a startup might opt for user-friendly cloud-based solutions like QuickBooks or Xero, which offer scalability as the business grows. Conversely, larger companies may require more robust software such as Sage or NetSuite, which provide extensive customization and advanced reporting features.

Factors to Consider:

Ultimately, the right system should support efficient workflow and provide accurate insights while being easy for your team to navigate.

Transitioning from a single-entry to a double-entry bookkeeping system can be a significant change for any business, but it can also be highly rewarding. To facilitate this process, planning and preparation are key.

By taking these steps, a business can mitigate the challenges of transitioning, allowing for a more seamless integration and enabling it to leverage the robust capabilities that double-entry bookkeeping offers for financial accuracy and reporting.

As we wrap up the discussion on single-entry and double-entry bookkeeping systems, it is evident that both methods have their unique offerings tailored to different business needs. Single-entry bookkeeping may cater well to small businesses with straightforward finances, enabling easy tracking of income and expenses. However, the limitations of this method, especially in accuracy and financial insight, can become apparent as businesses grow and require more complex reporting.

On the other hand, double-entry bookkeeping lays the foundation for financial accuracy and detailed reporting. It addresses error detection and prevention effectively while providing meaningful insights vital for strategic decisions. As businesses evolve, adopting a more sophisticated double-entry system can unlock the potential for better financial management and compliance.

To maximize the benefits of a chosen bookkeeping system, consider these best practices:

Overall, whether you choose single-entry or double-entry bookkeeping, the key lies in commitment to accuracy, transparency, and efficient processes. By following these best practices, businesses can cultivate a strong financial foundation that supports their growth and future success.