Importance of Bookkeeping for Small Businesses

Definition of Bookkeeping

Bookkeeping can be defined as the systematic recording of financial transactions in a business. It involves tracking all monetary exchanges, including sales, purchases, receipts, and payments. For small business owners, it’s not just about keeping track of numbers; it’s the backbone of financial management. Imagine trying to navigate a new city without a map—without bookkeeping, that’s how a business might feel when managing finances.

Significance of Accurate Bookkeeping

Accurate bookkeeping is crucial for small businesses for several reasons:

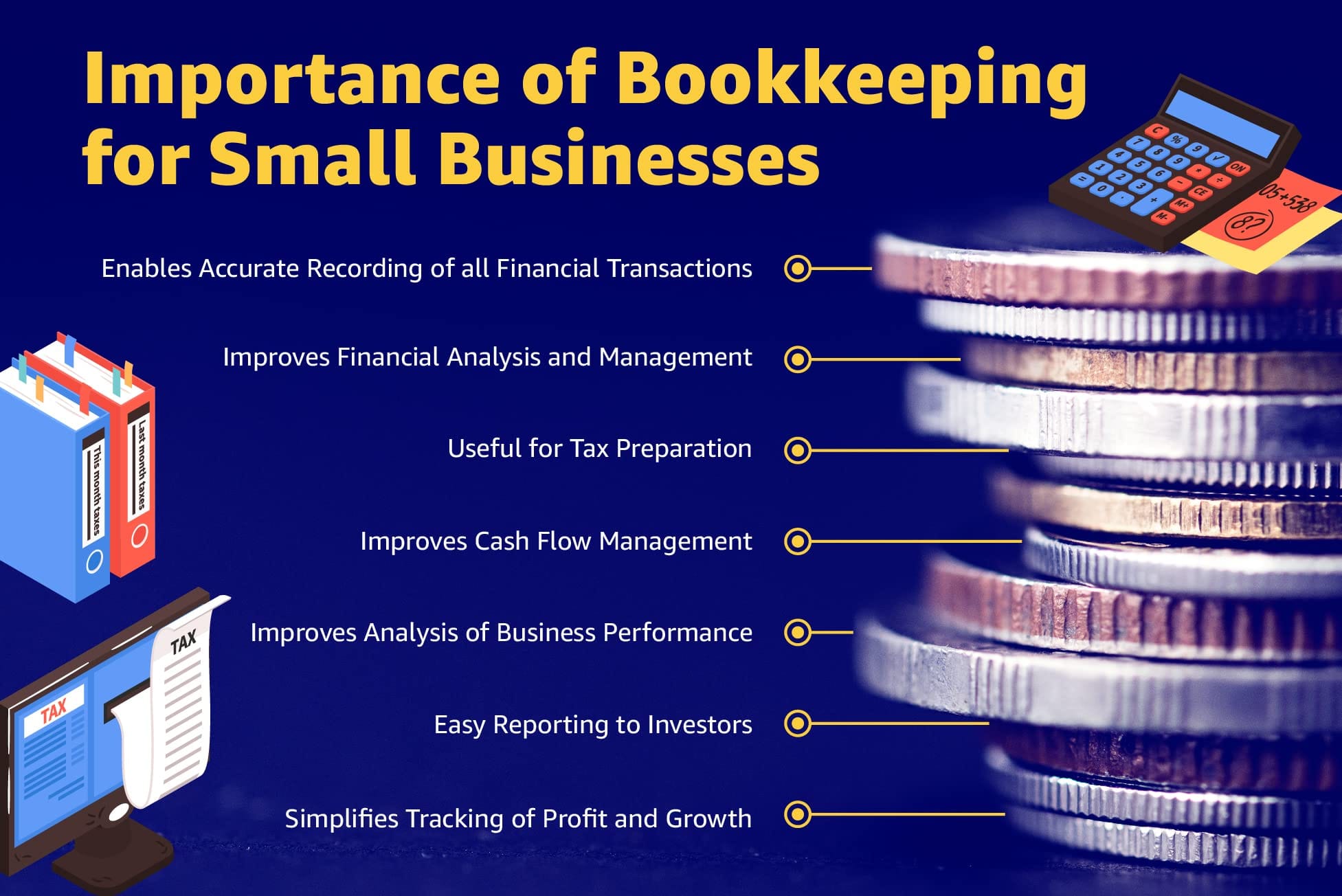

- Financial Health Monitoring : It enables owners to understand the financial position, cash flow, and profitability of their business.

- Informed Decision Making : With accurate records, business owners can make strategic decisions, like when to expand, downsize, or invest in new opportunities.

- Tax Readiness : An organized bookkeeping system makes tax preparation smoother and ensures compliance with tax laws, minimizing the risk of audits or penalties.

- Investor Confidence : For those seeking investment, having well-kept books demonstrates professionalism and builds trust.

A personal anecdote—one small business owner shared how they avoided financial disaster by locating discrepancies through diligent bookkeeping. This practice not only salvaged their funds but also opened up avenues for growth they hadn’t considered before.

In conclusion, understanding bookkeeping is foundational for the longevity and success of a small business. It’s more than just a chore; it’s a strategic tool that empowers business owners.

Benefits of Effective Bookkeeping

Financial Analysis and Decision Making

Effective bookkeeping offers small business owners a treasure trove of benefits, especially in the areas of financial analysis and decision-making. By maintaining accurate records of financial transactions, businesses can gain vital insights into their performance.

For example:

- Budgeting : Business owners can analyze past expenses to create realistic budgets for the future.

- Trend Identification : With organized data, it’s easier to spot sales trends, allowing businesses to capitalize on peak buying periods.

- Cash Flow Management : Accurate bookkeeping can help track when money enters and exits your business, highlighting potential shortfalls before they become critical.

Ultimately, this analytical foundation helps in making informed decisions that can propel the business forward.

Tax Compliance and Reporting

When it comes to tax compliance and reporting, effective bookkeeping is nothing short of essential. Accurate financial records serve as a reliable reference for tax filings, ensuring:

- Timely Submissions : With organized documentation, businesses can file taxes on time, avoiding penalties.

- Audit Preparedness : By having precise records, businesses can easily provide documentation if audited by tax authorities.

- Deductions Optimization : Good bookkeeping allows for meticulous tracking of expenses, maximizing eligible deductions and potentially lowering tax liabilities.

Consider a small café owner who learned to embrace thorough bookkeeping. Thanks to their organized financial records, they not only passed their tax audit with flying colors but also discovered deductible expenses they hadn’t considered, leading to significant tax savings.

In summary, effective bookkeeping lays the groundwork for strategic financial planning and smooth compliance with tax regulations, making it an indispensable asset for any small business.

Bookkeeping Methods for Small Businesses

Single-Entry Bookkeeping

As small business owners dive into the world of bookkeeping, understanding the different methods available can simplify their financial management. One of the simplest approaches is single-entry bookkeeping. This method is ideal for smaller operations that have straightforward financial transactions.

In single-entry bookkeeping, each transaction is recorded just once, primarily in a cash book. For instance, if a business makes a sale, it only notes the revenue. This method is often characterized by:

- Easy-to-understand, minimalist approach

- Suitable for tracking daily cash flow

- Lower initial setup costs

However, it does have limitations. With only one entry per transaction, it’s difficult to capture the full financial picture, which can lead to oversight.

Double-Entry Bookkeeping

On the other hand, double-entry bookkeeping is a more comprehensive and widely used system, especially for growing businesses. Each transaction is recorded in two accounts: a debit in one, and a credit in another, ensuring the accounting equation (Assets = Liabilities + Equity) always balances.

The advantages of double-entry bookkeeping include:

- Enhanced accuracy due to checks and balances

- Better financial insights, supporting more informed decisions

- Easier identification of errors and discrepancies

For instance, a retailer selling inventory would record the sales revenue and decrease inventory simultaneously, providing a complete view of the transaction. A friend who owns a growing e-commerce store swears by double-entry, stating it has saved them countless headaches during tax season due to the clarity it provides.

In short, choosing the right bookkeeping method relies on the complexity and scale of the business, with single-entry being suitable for smaller operations and double-entry offering a robust solution for those seeking growth.

Importance of Bookkeeping for Small Businesses

When it comes to running a small business, several factors determine success or failure. One critical aspect that shouldn’t be overlooked is bookkeeping. It may sound mundane, but effective bookkeeping is the backbone of any healthy business operation.

Understanding Financial Health

At its core, bookkeeping provides a clear picture of a company’s financial health. It tracks income and expenses meticulously, enabling business owners to make informed decisions. For instance, a small café owner can identify their peak sales days and adjust staffing or inventory accordingly, maximizing profit and efficiency.

Compliance and Tax Readiness

Additionally, proper bookkeeping ensures compliance with local laws and helps prepare for tax season. A well-maintained set of books means less stress when it’s time to file taxes. Business owners who dedicate time to detailed bookkeeping can avoid hefty fines and penalties related to tax misfiling.

Building Stronger Relationships

Moreover, effective bookkeeping fosters better relationships with stakeholders. Investors and banks prefer to see accurate financial records, which can lead to easier access to funding or loans when needed.

In summary, bookkeeping is not just a task; it’s a vital part of strategic planning that enables small businesses to thrive in a competitive landscape. Abandoning this practice can lead to disastrous consequences, often catching business owners off guard.

Benefits of Effective Bookkeeping

Transitioning from the critical importance of bookkeeping, let’s delve into the specific benefits that effective bookkeeping brings to small businesses. It’s not just about recording financial transactions; it’s about evolving your business strategy through data.

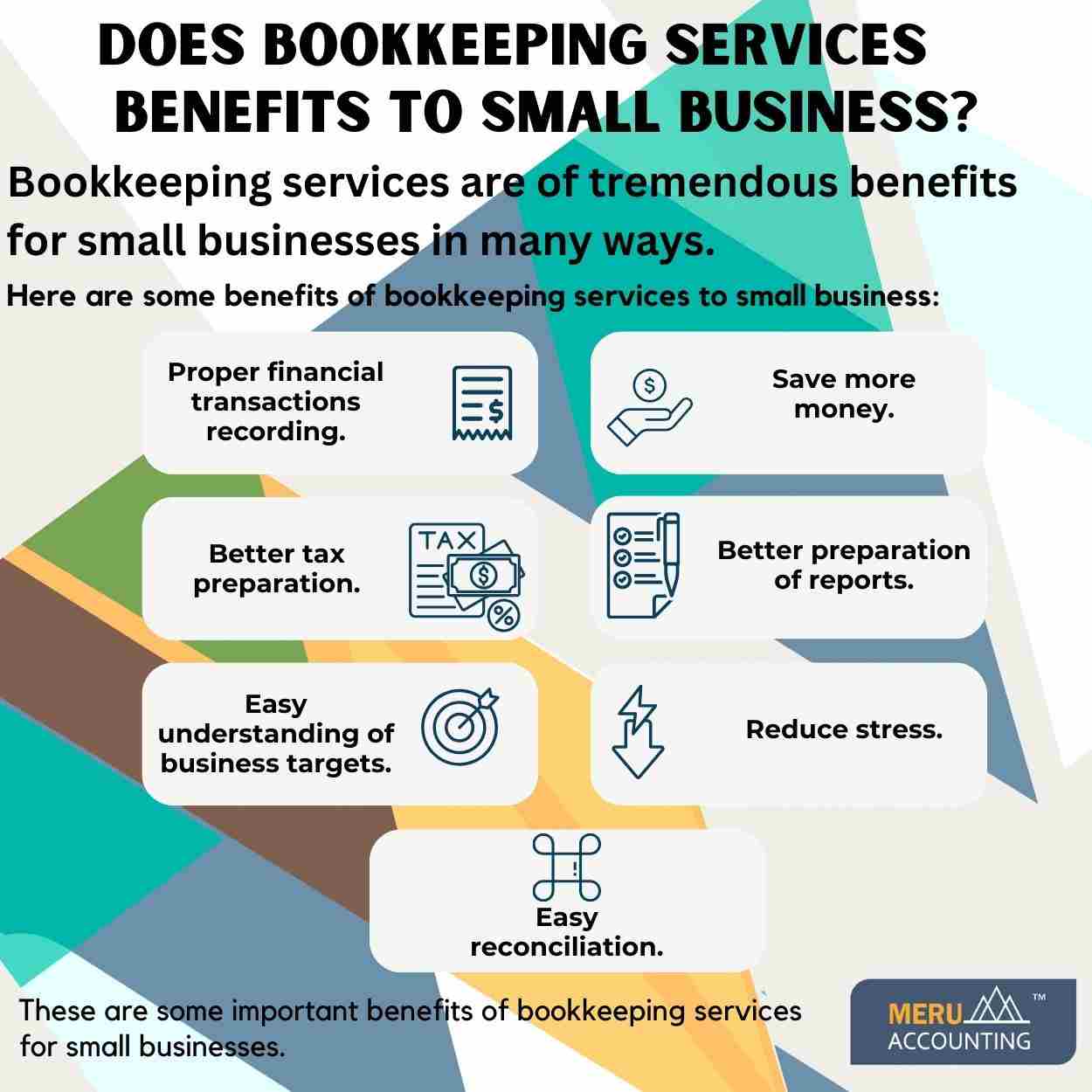

Improved Financial Management

One of the primary benefits of effective bookkeeping is improved financial management. Accurate records enable business owners to understand their cash flow better and spot trends over time. For instance, a local boutique can track their expenses and income to determine which products are bestsellers and which ones may not be worth restocking.

Enhanced Decision-Making

Another vital advantage is enhanced decision-making. With access to timely financial data, business owners can make quick, informed decisions—whether that means investing in new equipment, hiring staff, or launching a promotional campaign.

Budgeting Made Easier

Effective bookkeeping also simplifies the budgeting process. Business owners can set realistic budget targets based on past performance, helping them to forecast revenues and expenses accurately.

Time and Cost Efficiency

Lastly, having well-organized financial records saves time and money. Instead of scrambling at tax time or during audits, a well-maintained bookkeeping system allows for seamless reporting and retrieval of information, ultimately leading to reduced administrative costs.

In summary, effective bookkeeping transforms raw data into valuable insights, allowing small businesses to make strategic choices that foster growth and sustainability.

Bookkeeping Methods for Small Businesses

Building on the benefits of effective bookkeeping, understanding the various methods available is crucial for small business owners. Different methods can tailor to different business needs, providing unique advantages.

Single-Entry Bookkeeping

One common method is single-entry bookkeeping. This simple approach records each financial transaction as either an income or an expense without maintaining a detailed double-entry system. This is especially useful for sole proprietors or very small businesses. For example, if a freelance graphic designer only needs to track income from clients and expenses for software, single-entry could suffice.

Double-Entry Bookkeeping

On the other hand, double-entry bookkeeping is a more comprehensive method that records every transaction in two accounts: a debit and a credit. This method offers a more accurate depiction of a business’s financial situation. For instance, if a small restaurant purchases new kitchen equipment, the cost is recorded as an asset (debit) and a reduction in cash (credit), ensuring balanced records.

Cloud-Based Bookkeeping

Today, many small businesses opt for cloud-based bookkeeping software that integrates various functions like invoicing, expense tracking, and financial reporting. This method not only streamlines processes but also allows for real-time collaboration between team members and accountants.

Selecting the right bookkeeping method can profoundly impact daily operations, decision-making, and long-term success. Evaluating which method best aligns with the business’s needs is essential for establishing a solid financial foundation.

Tools and Software for Bookkeeping

Having explored bookkeeping methods, it’s clear that the right tools and software can significantly enhance the efficiency and accuracy of bookkeeping practices. With so many options available, choosing the right one can amplify a business’s financial management.

Popular Bookkeeping Software

One of the most popular tools in the industry is QuickBooks. This user-friendly software offers various features, from expense tracking to invoicing and financial reporting. A local bakery owner mentioned how using QuickBooks simplified her tax preparation, allowing her to focus more on baking than balancing books.

Cloud-Based Solutions

For those who prefer cloud-based solutions, Xero is a solid option. It provides real-time access to financial data from anywhere, facilitating collaboration among team members. Imagine a small marketing agency that needs to review budgets on-the-go; with Xero, they can pull up the necessary data anytime.

Free Alternatives

Don’t overlook free alternatives, either. Wave Accounting offers impressive features without the price tag, making it an excellent choice for startups. With its easy-to-navigate interface, entrepreneurs can manage finances without getting bogged down by complex processes.

Integrative Tools

Lastly, many businesses benefit from using integrative tools, such as Expensify for expense reporting or Shopify for e-commerce. These tools sync with main accounting software, keeping everything organized without manual entry.

In summary, leveraging the right bookkeeping tools can greatly improve the financial health of a small business, allowing owners to focus on growth and customer relationships rather than getting lost in paperwork.