Introduction

Definition of Bookkeeping Terminology

Bookkeeping terminology encompasses the specific language and jargon used in the field of accounting. Understanding these terms is crucial for anyone involved in managing finances, whether for a business or personal use. Here are a few core terms:

- Assets: Resources owned by a business that provide future economic benefits.

- Liabilities: Obligations that a business owes to outside parties.

- Equity: The residual interest in the assets of a business after deducting liabilities.

These terms form the backbone of financial reporting and help convey a company’s financial health.

Significance of Understanding Bookkeeping Terms

Understanding bookkeeping terms is not just an academic exercise; it is essential for effective financial management. For example, when a small business owner learns the difference between accounts payable and accounts receivable, they can better manage cash flow.

In an increasingly complex financial landscape, grasping these concepts allows individuals and businesses to:

- Make informed decisions.

- Communicate effectively with accountants and financial analysts.

- Prepare accurate financial statements and reports.

By mastering these terms, one can enhance their financial literacy and confidently navigate the world of bookkeeping.

Foundation of Bookkeeping

Double-Entry Accounting

At the heart of effective bookkeeping lies the principle of double-entry accounting. This method ensures that every financial transaction affects at least two accounts, which can help maintain balance in a business’s financial records. For instance, when a company makes a sale, it not only records the income but also increases its inventory cost.

The beauty of this system is in its checks and balances, as it requires that:

- Debits equal Credits: For every entry made, there is a corresponding and opposite entry.

- It minimizes the chances of errors, safeguarding the integrity of financial reporting.

Chart of Accounts

Next up is the chart of accounts, a tool that serves as a roadmap for an organization’s financial transactions. It categorizes all accounts in the general ledger, making it easier to organize financial information efficiently.

Typically structured in a list, it may include:

- Assets: Cash, Inventory, Equipment

- Liabilities: Loans, Accounts Payable

- Equity: Owner’s Capital, Retained Earnings

- Revenue: Sales Income, Service Income

- Expenses: Rent, Utilities, Salaries

Having a clear chart of accounts simplifies tracking and reporting, making it an invaluable component of a successful bookkeeping foundation. Understanding both double-entry accounting and the chart of accounts is essential for anyone looking to master bookkeeping and maintain accurate financial records.

Common Bookkeeping Terms

Debits and Credits

Understanding debits and credits is crucial in the world of bookkeeping. Think of them as the heartbeat of your financial transactions. In a double-entry accounting system, every time you record a debit, there’s a corresponding credit to ensure balance.

For example:

- Debit: Increases an asset or expense account.

- Credit: Increases a liability or income account.

This dual entry not only keeps accounts balanced but also provides a comprehensive view of financial health.

Accounts Payable vs. Accounts Receivable

Next, let’s delve into accounts payable and accounts receivable, two sides of the same coin in business finance.

- Accounts Payable: This represents the money a company owes its suppliers. For example, when you order new office supplies on credit, that amount goes into accounts payable until it’s paid off.

- Accounts Receivable: Conversely, this refers to the money clients owe the business for services rendered or products sold. For instance, if you’ve invoiced a client, that invoice represents accounts receivable until paid.

Understanding the difference helps manage cash flow effectively, ensuring the business remains solvent and can meet its obligations.

Assets, Liabilities, and Equity

Finally, we have the foundational elements: assets, liabilities, and equity. These terms describe a company’s financial position:

- Assets: Valuable resources owned by the business, such as equipment, cash, and real estate.

- Liabilities: Obligations that the company must pay to others, like loans and unpaid bills.

- Equity: The owner’s stake in the company, reflecting ownership after all liabilities are settled.

Overall, mastering these common bookkeeping terms helps individuals and businesses navigate their financial landscape with greater ease and accuracy. Understanding these concepts is essential for making strategic decisions that drive success.

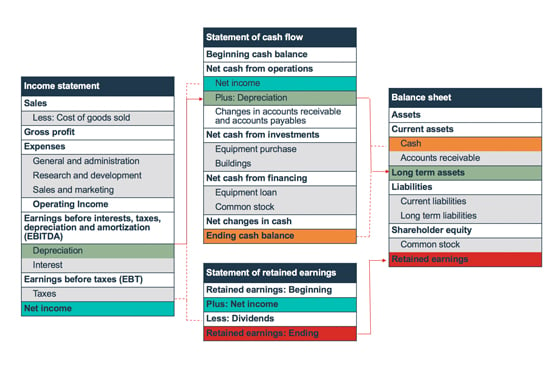

Financial Statements

Balance Sheet

Diving deeper into the realm of bookkeeping, financial statements play a vital role in showcasing a business’s performance. The balance sheet is one of the key financial statements that captures a snapshot of a company’s financial position at a specific point in time. It lists assets, liabilities, and equity, conveying whether the business is solvent.

To visualize:

- Assets: Cash, Accounts Receivable, Inventory

- Liabilities: Loans, Accounts Payable

- Equity: Owner’s Capital, Retained Earnings

Knowing this can help managers and investors make sound financial decisions.

Income Statement

Next is the income statement, sometimes called the profit and loss statement, which summarizes the revenues and expenses over a specific period, typically quarterly or annually. This statement evaluates operational efficiency and profitability.

Key components include:

- Revenue: Total sales or services provided.

- Expenses: Costs incurred during the period, like rent and salaries.

- Net Income: The bottom line, showing profit or loss.

For example, a business that tracks income against expenses can identify trends and adjust operations accordingly to ensure profitability.

Cash Flow Statement

Finally, the cash flow statement offers insights into the movement of cash in and out of the business, highlighting liquidity. It’s essential for understanding how cash is generated and used in various activities:

- Operating Activities: Cash transactions related to core business operations.

- Investing Activities: Cash used in or generated from investments.

- Financing Activities: Cash transactions involving borrowing or repaying debts.

A solid grasp of these three financial statements—balance sheet, income statement, and cash flow statement—empowers business owners and stakeholders to gauge financial health, make informed decisions, and plan for the future effectively.

Bookkeeping Methods

Accrual Accounting

Transitioning from financial statements, it’s essential to explore the different methods of bookkeeping that businesses can adopt. Accrual accounting is one of the most widely used methods. This approach records revenue and expenses when they are earned or incurred, rather than when the cash changes hands.

For instance, if you provide a service in March but receive payment in April, the income is recorded in March, allowing for a more accurate picture of financial performance for that period. Key benefits of accrual accounting include:

- Better matching of income and expenses.

- Comprehensive financial visibility.

- Enhanced decision-making capabilities based on complete data.

While it can be more complex, especially for smaller businesses, it generally provides a clearer financial picture over time.

Cash Accounting

On the flip side, we have cash accounting, a simpler method that records transactions only when cash is exchanged. This method is particularly popular among small businesses and freelancers due to its straightforward nature.

Imagine a situation where you perform a service in February and get paid in March. Under cash accounting, the revenue would be recorded in March, reflecting actual cash on hand. Key features include:

- Simplicity in tracking cash flow.

- Immediate recognition of income and expenses.

While it offers easier record-keeping, cash accounting may not provide as accurate a long-term view of the business’s financial health. Understanding the distinctions between these two methods allows business owners to choose the most suitable bookkeeping practice based on their specific needs and goals.

Recording Transactions

Journal Entries

Continuing from bookkeeping methods, a crucial step in managing finances is recording transactions. The first phase of this process is creating journal entries. Each entry details a financial transaction, capturing essential information like the date, accounts affected, and amounts.

For example, if a business purchases $500 worth of office supplies, the journal entry would look something like this:

- Date: [Transaction Date]

- Debit: Office Supplies $500

- Credit: Cash/Accounts Payable $500

This structured format ensures clarity and allows for easy tracking of all transactions over time.

General Ledger

Once journal entries are recorded, they are posted to the general ledger, which serves as a comprehensive record of all financial transactions. The general ledger organizes transactions by account, making it easier to generate reports and analyze the financial status of the business.

For instance, each account (like cash, revenue, and expenses) will reflect all related journal entries, providing a complete picture. The benefits of maintaining an organized general ledger include:

- Enhanced accuracy in financial reporting.

- Simplified preparation of financial statements.

- Better insights into financial patterns over time.

Mastering the process of recording transactions through journal entries and maintaining a general ledger is essential for effective bookkeeping and ensures that business owners have a clear view of their financial landscape.

:max_bytes(150000):strip_icc()/ratioanalysis-Final-6b8f05a58b3e4a8b9055000cb874305d.jpg)

Financial Analysis

Ratio Analysis

As we delve deeper into effective financial management, financial analysis is crucial for comprehending a business’s performance and making informed decisions. One powerful tool in this realm is ratio analysis. This technique evaluates financial metrics to highlight strengths and weaknesses in the company.

Key ratios often include:

- Liquidity Ratios: Assessing short-term financial stability, like the current ratio (current assets/current liabilities).

- Profitability Ratios: Measuring how efficiently a company generates profit, such as the net profit margin (net income/revenues).

- Leverage Ratios: Understanding the extent of debt a company holds, like the debt-to-equity ratio (total liabilities/shareholder equity).

By examining these ratios, business owners can pinpoint areas for improvement and gauge overall financial health.

Budgeting

Following ratio analysis, we have budgeting, another critical component of financial analysis. A budget serves as a financial roadmap, allowing businesses to plan and allocate resources effectively.

Creating a budget involves:

- Setting financial goals, such as increasing sales or reducing expenses.

- Estimating revenues and determining how much can be spent across various business areas.

By regularly comparing actual performance against the budget, businesses can make real-time adjustments to stay on track financially. This proactive approach not only fosters accountability but also enables companies to identify trends and plan for future growth. Mastering both ratio analysis and budgeting equips business owners with the insights needed to thrive in a competitive landscape.

Software and Tools

Importance of Bookkeeping Software

Shifting gears into the realm of technology, the use of bookkeeping software is vital for modern financial management. These tools streamline processes, enhance accuracy, and save valuable time. Imagine having an easy-to-use platform that automatically tracks expenses, generates financial reports, and ensures compliance with regulatory standards—all at your fingertips.

The importance of bookkeeping software can be seen in several benefits:

- Automation: Eliminates repetitive tasks, allowing for faster data entry and report generation.

- Real-time tracking: Provides up-to-date financial insights, empowering quicker decision-making.

- Improved accuracy: Reduces human error, ensuring more reliable financial records.

With tailored solutions to fit business needs, investing in bookkeeping software can significantly ease workload and enhance financial clarity.

Popular Bookkeeping Tools

When it comes to choosing bookkeeping software, several popular tools stand out in the market:

- QuickBooks: Renowned for its user-friendly interface and extensive features, suitable for small to medium-sized businesses.

- Xero: Offers robust reporting capabilities and is particularly favored by accountants.

- FreshBooks: Designed with freelancers in mind, it focuses on invoicing and expense tracking.

These tools do more than just record incidents; they offer insights that guide strategic planning. Whether you’re a small business owner or a freelancer, leveraging the right bookkeeping tools can elevate your financial management, allowing you to concentrate on growth and success.

Compliance and Regulations

GAAP (Generally Accepted Accounting Principles)

As we navigate the world of bookkeeping, understanding compliance and regulations is essential for maintaining financial integrity. A cornerstone of this is GAAP (Generally Accepted Accounting Principles). These guidelines outline the standard framework of accounting practices used in the United States, ensuring consistency and transparency in financial reporting.

Some key principles of GAAP include:

- Consistency: Businesses must maintain consistent accounting methods to provide clearer trend analysis over time.

- Relevance: Financial statements should provide information useful for decision-making.

- Reliability: Information must be accurate and verifiable.

Adhering to GAAP not only aids in compliance but also builds trust with investors and stakeholders, fostering a solid reputation in the marketplace.

Tax Deductions and Reporting

In addition to GAAP, understanding tax deductions and reporting is vital for any business operating within legal bounds. Accurate bookkeeping allows businesses to identify eligible deductions that can reduce taxable income, ultimately saving money.

Common tax deductions include:

- Business expenses: Office supplies, utilities, and rent.

- Vehicle expenses: Costs associated with business-related travel.

- Employee wages: Payments made to employees can often be deducted.

It’s equally important to ensure timely and accurate tax reporting to avoid penalties. Regularly updating bookkeeping records can simplify this process and provide confidence during tax season. By mastering compliance with GAAP and understanding tax implications, business owners can navigate the financial landscape more effectively, ensuring sustainability and growth.

Conclusion

Recap of Essential Bookkeeping Terms

As we wrap up our exploration of bookkeeping, it’s crucial to recap the essential terms and concepts we’ve covered. From understanding the basics of debits and credits to the intricacies of financial statements and compliance regulations, these elements form the backbone of effective financial management. Key terms include:

- Assets, Liabilities, and Equity: The core components of a balance sheet.

- Journal Entries and General Ledger: Critical for recording transactions and maintaining accurate records.

- GAAP: Ensuring adherence to established accounting principles.

Each of these terms plays a vital role in helping business owners better understand their financial positions.

Final Insights

Ultimately, mastering bookkeeping is not just about numbers; it’s about telling the financial story of your business. Leveraging technology, such as bookkeeping software, and adhering to compliance standards ensures that you stay on top of your financial game.

The knowledge gained through this guide empowers you to make informed decisions, plan strategically, and foster growth. Embracing these financial fundamentals can set the stage for a thriving business journey ahead. Remember, every financial detail counts—so keep refining your bookkeeping practices for lasting success!